Government’s Frugal Borrowing Strategy: A Boon for Bond Markets

The recent revelation of the central government’s restrained borrowing plans for the first half of the fiscal year has ignited a wave of optimism in bond markets. Here’s why this move carries significant weight:

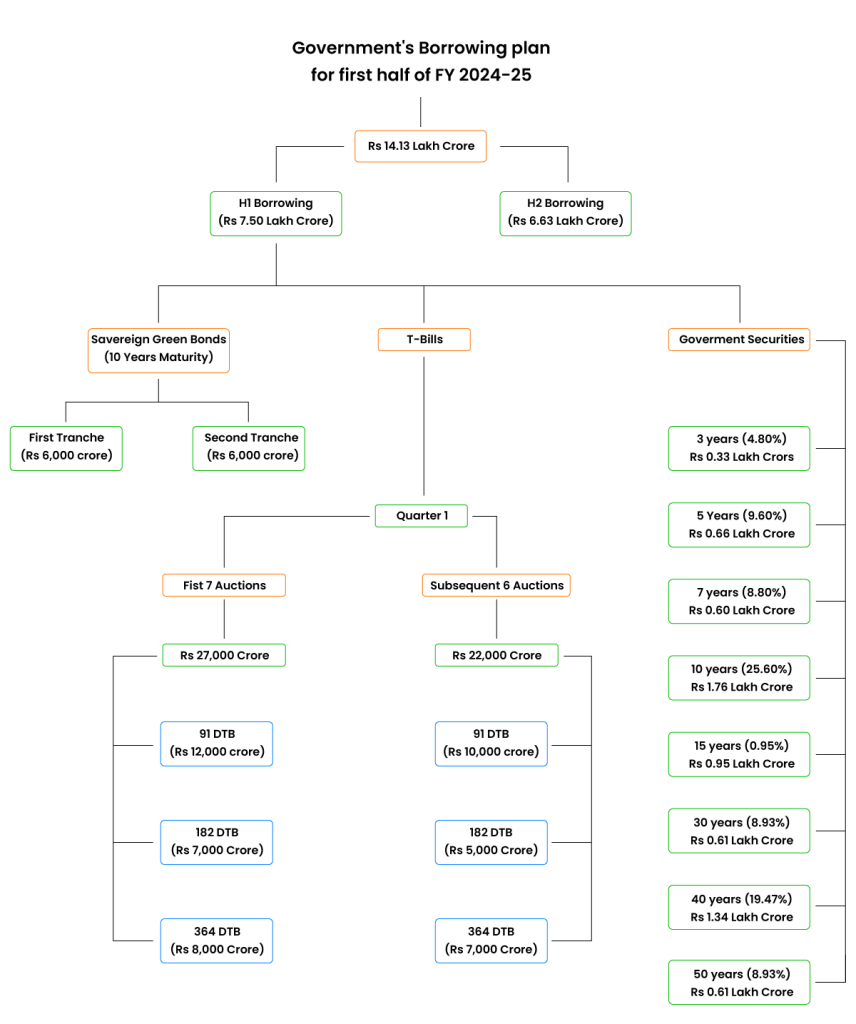

- Unexpected Borrowing Reduction: The government’s decision to borrow substantially less than market projections, slashing around INR 75k from expectations, has turned heads in the investor community. With only 53% of the annual borrowing earmarked for the initial half, it marks a considerable downturn, instilling newfound confidence.

- Innovative Maturity Offerings: By introducing novel maturity options like the 15-year and 50-year bonds, the government aims to broaden its appeal to a diverse array of investors. This strategic maneuver enhances the allure of government bonds, catering to varying investor preferences.

- Proactive Liquidity Management: The Reserve Bank of India’s proactive liquidity maneuvers have culminated in a favorable shift in the operative rate, rendering borrowing more cost-effective. This, coupled with relaxed liquidity conditions, is poised to fuel heightened investor demand.

- Tailoring to Investor Dynamics: The borrowing calendar has been meticulously crafted to synchronize with evolving investor dynamics. By adjusting supply to accommodate factors such as anticipated FPI flows, real money investor sentiment, and dynamic bank valuation guidelines, the government endeavors to maintain equilibrium in the market landscape.

Impact on Markets:

Amidst this backdrop of fiscal prudence and strategic maneuvering, the impact on bond markets is poised to be profound:

- Bullish Momentum in Bonds: An anticipated uptick of 5-10 basis points across the bond spectrum signals an initial rally, fueled by diminished supply and enhanced liquidity conditions.

- Potential Curve Dynamics: Initial reactions may manifest in curvature, particularly in maturity brackets up to 7 years. However, long-duration bonds are anticipated to emerge as frontrunners in the quest for yield.

- Forecasted Spread Compression: As government bonds rally, expectations of spread compression in corporate bonds and state government securities (SDL) during Q1 are on the horizon. This trend is driven by improved liquidity conditions and a contraction in supply.

In essence, the government’s prudent fiscal stance sets the stage for a promising trajectory in bond markets, offering investors a blend of stability, adaptability, and growth potential.

Leave a Reply