Choosing Between Tax Regimes: Making the Right Decision

Navigating through the complexities of tax regimes can often be daunting, especially when faced with the decision between the old and the new tax regime. With the Indian government’s introduction of the new tax regime in recent years, taxpayers are presented with a crucial choice that could significantly impact their financial planning and obligations. This decision requires a thoughtful analysis of various factors, ranging from individual financial goals to potential tax benefits and implications. Delving into this decision-making process demands a comprehensive understanding of both tax structures and their respective nuances. Hence, embarking on the journey to determine which tax regime best aligns with one’s financial objectives necessitates careful consideration and informed decision-making.

The 2023 Budget stirred up confusion among taxpayers about whether to stick with the old tax rules or switch to the new ones. The government added some perks in the budget to encourage folks to go for the new system. It seems like they want everyone to move over to the new way eventually, but they’re keeping the old system in place for now. So, even though the new rules are the main choice for now, you still have the option to go with the old ones if you like.

Deciphering Taxes: Which Route to Take?

In the wake of the 2020 Budget, a revamped tax scheme emerged, reshaping the landscape of tax brackets and offering reduced rates to taxpayers. However, this new arrangement came with a trade-off: opting for the updated regime meant forfeiting a range of familiar benefits, including exemptions for HRA, LTA, as well as deductions under sections 80C and 80D. Consequently, the allure of the new tax system failed to capture the interest of many taxpayers.

Here’s what’s different about the new tax regime.

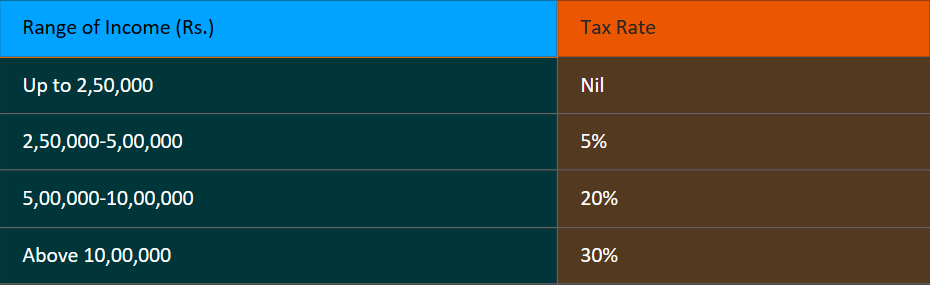

- The new system introduces six tax slabs, compared to the previous four. Essentially, tax slabs now extend up to 3 lakhs, with zero tax applicable for income up to this amount.

- Tax deductions and exemptions are no longer part of the new tax regime. While the old system offered 70 options for tax savings, potentially allowing for savings of up to 10.25 lakhs, the new regime simplifies this to just a handful of options. Under the new system, taxpayers can benefit from reduced taxes even without investing in tax-deductible schemes.

- Like the old regime, a standard deduction of Rs 50,000 remains applicable in the new system.

- In the new regime, tax rebate applies to income up to Rs 7.5 lakhs, providing relief for taxpayers who previously paid no tax up to this income level.

The following table helps us understand Tax slabs Under New Regime :

Old Tax Regime

Before the advent of the new tax regime, there existed the old system, which offered a multitude of tax-saving avenues. With over 70 exemptions and deductions at hand, including benefits such as HRA and LTA, taxpayers could effectively reduce their taxable income, consequently lowering their tax liabilities. Among these, Section 80C stood out as the most popular and generous deduction, permitting a deduction of taxable income of up to Rs. 1.5 lakh. Presently, taxpayers are presented with a choice between embracing the old or new tax regime.

The following table tells us about the old regime and its tax slabs

New vs. Old Tax Regimes: Making the Right Choice

The choice to transition between the new and old tax regimes hinges on various factors such as:

- Income bracket – In the recently updated tax system, the tax rates have been lowered compared to the previous structure. This adjustment could be particularly advantageous for individuals with higher incomes. For example, according to the 2023 budget, someone earning INR 9 lakh annually would now owe INR 45,000 in taxes, which is 5% of their taxable income. This marks a significant decrease from the previous tax burden of INR 92,500 under the old tax system. Similarly, for individuals earning INR 15 lakh annually, their tax liability would decrease to INR 1.5 lakh under the new tax rates introduced in the 2023 budget. This reduction contrasts with the previous tax obligation of INR 1.87 lakh calculated under the earlier tax system’s rates before the 2023 budget. The lowered tax liabilities result from the implementation of reduced tax rates in the new tax system, which has revised tax brackets and rates to ease the burden on taxpayers.

- Financial objectives – Before deciding on a tax regime, it’s important to assess your investment objectives. The new tax system is preferable if you’re open to flexible investment options and aren’t planning to invest in tax-saving schemes. However, if you have specific investment goals like retirement planning or accumulating funds for long-term objectives, the old tax regime might be more advantageous. This is because it provides deductions for contributions made to different investment vehicles.

- Tax breaks and exemptions – Under the former tax system, individuals could benefit from a deduction of Rs 1.5 lakh under Section 80C and Rs 2 lakh under Section 24(b) for self-occupied property interest. This allowed for a total deduction of Rs. 3.5 lakh under the old tax regime, a feature not present in the new tax system.

Conclusion –

In conclusion, the decision of which tax regime to choose ultimately depends on individual financial circumstances, goals, and preferences. While the new tax regime offers simplified tax rates and fewer deductions/exemptions, it may be more beneficial for those seeking flexibility in investments and willing to forgo certain tax-saving options. Conversely, the old tax regime provides a broader range of deductions and exemptions, making it advantageous for individuals with specific investment goals, such as retirement savings or long-term wealth accumulation. Therefore, taxpayers should carefully evaluate their financial objectives and consult with financial advisors to determine the most suitable tax regime for their needs, ensuring optimal tax planning and financial well-being.

Leave a Reply